Regional Outlooks

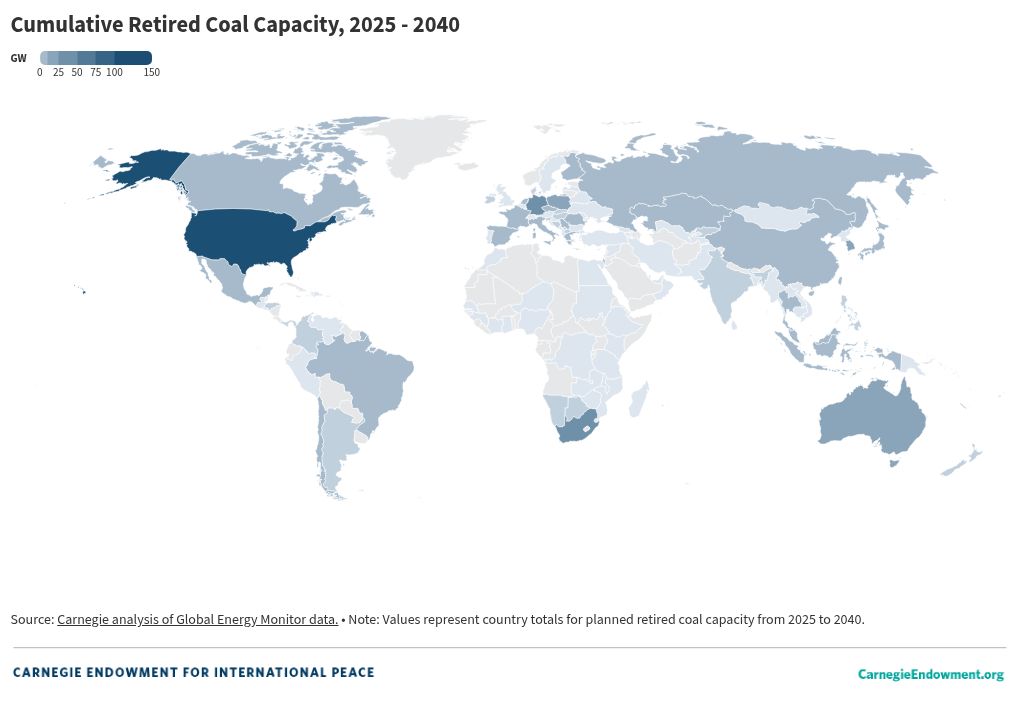

The United States has the largest quantity of repurposing projects of any country. Converting coal plants to natural gas has been ongoing since the shale boom in 2010, but the clean power conversion is a newer story, likely spurred by a confluence of ambition from utilities and recent policy support: The 2022 Inflation Reduction Act offers “bonus” incentives for projects in retired coal power plants. State policies could also have impact. For example, Illinois’ Coal-to-Solar program offers grants to nine solar and storage repowering projects. Although geographically diverse, most of the U.S. repowering projects are primarily batteries and solar, followed by synchronous condensers. There are only a small handful of bioenergy, nuclear, and hydrogen-based projects, including some natural gas plants that are H2-ready. The United States is a key market to watch given potential policy shifts: Retired coal plants could be repurposed as gas plants or paused altogether.

Europe contributes more projects to the tracker than the United States—with sixty-seven repurposing efforts—and deploys a broader array of conversion technologies. European national coal retirement mandates are propelled by clean power incentives, carbon prices, and some direct repurposing funding. Although Europe has more wind repurposing projects than the United States, less than half of Europe’s developments are purely green. Several countries, including Germany, Denmark, and Hungary, have notably grey conversion pathways with an overreliance on biomass or hydrogen-ready natural gas. The UK’s successfully retired coal fleet has yielded a strong array of eight green projects but includes some controversial, high-emitting biomass. The Iberian Peninsula is home to several all-of-the-above projects with multiple generation and storage technologies alongside hydrogen and manufacturing facilities. This hub approach could carve an interesting path for Europe given its joint goals of decarbonization and industrial competitiveness.

Australia, Chile, and South Africa contain most of the remaining green conversions, with some sparse developments across other countries. Twelve of the fifteen Australian repurposing sites include batteries, as well as the largest share of long-duration energy storage projects of any country. The storage strategy, as well as some repowering projects, are supported in part by dedicated funding from the Australian Renewable Energy Agency. Chile’s top-down strategy to retire its coal fleet has been driven by thriving renewable growth and multilateral funding to stimulate four notable repurposing projects, including a novel molten salt battery. Although South Africa has three projects—all remnants of the Just Energy Transition Partnerships—only the Komati Power Station has made tangible progress toward its goals of deploying renewables and long-duration storage.

India and China each have only one green repurposing project, but they are essential countries to watch, given their enormous coal capacities and increasing clean power and storage installations. China recently announced support for its first-ever repurposing of a coal power plant with renewables and battery storage.

Technology Trends

Energy storage is the clear front-runner of repurposing. Across all projects, eighty-three feature batteries, often paired with renewable energy generation and synchronous condensers for grid stability. Five projects implement thermal energy storage, centralized heating systems that supply an entire neighborhood, mostly in Europe. Renewables such as solar are the second-most-important trend, but initial results indicate substantially smaller levels of power output from onsite solar compared to fuel predecessors. To address some of these challenges, sites in the Iberian Peninsula, Germany, and Australia offer an all-of-the-above approach with multiple renewables, storage, and backup hydrogen. Onsite installations of electrolyzers—the machine that produces hydrogen from electricity—comprise the third-most-observed replacement technology.

A handful of sites focus on next-generation energy systems from nuclear power to advanced hydrogen and energy storage. Ten of the battery projects deploy long-duration energy storage batteries, which provide at least eight hours—if not days—of capacity. This is a boon for grids with larger shares of variable renewable power. Several nuclear power plants—specifically small modular reactors—are in preliminary planning stages on former coal plant sites in the United States, UK, Romania, and Poland. Even further from commercial viability, nuclear fusion projects in the United States and UK have selected repowered sites for their eventual deployments. In addition to nuclear, a first-of-a-kind super critical geothermal pilot project is underway in Nevada, and West Virginia is home to a novel pyrolysis technique for hydrogen production with graphite byproduct.

A smaller subset of false-start projects convert fossil-based combustion to hydrogen blending, ammonia co-firing, or biomass burning. These technologies achieve, at best, marginal reductions in emissions and, at worst, lock-in high-emitting investments. Beyond a handful of projects in Europe, many of these grey conversions arise in East and South Asia. Like South Africa, Vietnam’s projects remain preliminary, with a focus on bioenergy as a fuel swap. Japan and South Korea have both hedged their repurposing strategies on blending hydrogen products in existing thermal plants—a process that analysts view as thermodynamically, economically, and environmentally unsound. Some of the observed coal plants in these countries are enormous—4 or 6 GW—posing potential long-term challenges to repowering this scale of generation. Given limited biomass feedstock and clean hydrogen, these pathways remain unviable, barring breakthrough changes in clean hydrogen production.

The Future of Repurposing

Repurposing is well positioned to continue, thanks to advancements in new energy solutions, the aging of existing coal fleets, and the notion that energy security stems from resources that aren’t fuel-reliant. Solar and battery storage technologies will likely come down in cost, while geothermal and nuclear are having a renaissance, theoretically prompting higher generation for onsite clean repowering.

Over the next fifteen years, over 300 GW of coal could be retired across the world, with key opportunities expanding across Latin America and Southeast Asia. This repurposing research will identify effective policy, finance, and regulatory pathways to convert existing power stations for clean energy use while assessing the social and environmental impacts on communities. Future research will explore specific regional and technological case studies while expanding the scope of analysis about repurposing beyond the power sector. With every retirement is a clean opportunity.

For more, see the Carbon to Clean Tracker.